I work for myself. Do I need insurance?

If you are a business of any sort, then yes, you should have business insurance. It doesn’t matter if you’re working on your own, you have a team made up of a few friends, or you’re running a big shop. If you’re accepting payment for your goods or services, you’re a business.

Starting a business isn’t easy, so protecting your hard work is definitely something to think about.

Self-Employed Insurance Requirements

What kinds of workers need business insurance? All kinds. Here are a few that come to mind:

- Freelancers

- Consultants

- 1099ers

- Independent contractors

- Home-based businesses

- Entrepreneurs

- Startups

- Small business owners

- Mompreneurs

- New businesses

- Old businesses

- Side jobbers

- Solopreneurs

What types of business insurance do I need?

You’re probably thinking, “I don’t even know where to begin. Help!”

Don’t worry. The types of business insurance you need depends on the types of risk you face. That’s why the first step to figuring out what insurance policies to look for is figuring out what your business risks are. This is important to know before getting started, because it can affect what types of coverage you need and how much you’ll pay. The type of protection you need heavily relies on the line of work you do.

Every business has its own unique risks. Your insurance plan should protect you from liabilities that may arise from your business. This is where an insurance agent can help out big time.

Get a free business insurance consultation.

Elements that can affect risk include:

- Your industry

- Where you work

- The type of building you work in

- Your business assets

- Whether or not you’ve had insurance claims in the past

- How many employees you have (including part-time, full-time, contractors, and subcontractors)

- Interacting with the public

- An insurance underwriter will assess your risks and come back to you with a quote, including the rates and terms of the policy (or policies) that fits your business best.

Liability insurance for the self-employed

Liability means “risk”. Owning your own company has risks, and that’s why liability insurance is a great place to start for self-employed business owners. Three popular liability policies include general liability, professional liability, and cyber liability insurance.

General Liability Insurance

What is general liability insurance? Basically, a general liability policy covers your bases for many of the common things that can go wrong when you own a business. This policy will protect you from a financial loss if you happen to damage someone’s property, or someone injures themselves tripping over your equipment.

Property damage and bodily injury are not the only benefits of general liability insurance. Nonphysical risks, like personal and advertising injuries*, are also covered.

*Non-insurance speak: General liability also covers claims involving copyright infringement, slander, libel, and false advertising.

Not only that, if someone files a lawsuit against you, your court expenses, lawyer’s fees, damages, losses, and so on, may be covered.

Note: Defense costs are pretty much included in all policies, so keep that in mind.

Professional liability insurance

Not every business requires this type of insurance. However, if you provide expert services or advice for a living, it’s very important. People like designers, tech consultants or photographers can benefit greatly from professional liability insurance.

Professional liability insurance (also known as errors and omissions or E&O insurance) protects you in the event that a client claims your business made a mistake, was negligent, or failed to deliver a promised service.

Non-insurance speak: Professional liability is basically protection against an unhappy client. Yep, it’s that simple.

If you’re a consultant, you give advice for a living. If your advice results in any type of financial loss for your client, you may find yourself facing a lawsuit if your client is peeved enough.

That jerk of a client could very well sue you. Paying the damages would seriously hurt your pocket, but with professional liability insurance the fees would be taken care of.

Can we all agree that having someone else pay for very expensive, very crappy, situations is almost always better than paying out of your own personal pocket?

Note: We will refrain from making this point in every section.

Cyber liability Insurance

You might be thinking, “That sounds pretty intense. It’s probably only for big companies.” And if you are, you’re wrong. Cyber liability insurance protects any business in which a customer’s personal info may be stolen or exposed.

Okay, that does sound a little intense. But here’s the deal: Anyone who uses tech to do business should have a cyber policy And as for big companies– yes, they usually do have strong security systems in place.

And that’s exactly why, statistically, hackers go after smaller organizations. You should think about getting cyber liability insurance if your business handles sensitive customer data (even something as simple as credit card information).

Cyber liability has an assortment of benefits, but here are a few:

- Customer notification

- Forensics investigation

- Identity theft

- Credit monitoring

- Reputation management

- Third-party services

- Equipment for business interruption

- Cyber extortion

- Regulatory fines and legal costs

Business property insurance

This one’s pretty self-explanatory. Business property insurance protects… well, your business property. Pretty much all commercial property can be protected under this policy– from smartphones to computers, photography equipment, and even the office building itself.

Should something get damaged due to theft, fire, vandalism, natural disasters, or whatever, this policy will have your stuff covered. You can choose to have your policy pay for losses based on the replacement cost or actual cash value. For more on that, go here.

accident claim.

A very important note about home-based businesses and property damage

Home-based businesses often rely on their homeowners or renters insurance to cover their business items– 48% of home businesses, in fact.

Unfortunately, what some may find out a little too late is that those policies will typically only cover up to $500 in work-related damages. That’s why it’s very important to protect your commercial property.

Learn more about why home-based businesses need more than homeowners insurance.

I have work property, but I take it with me to meetings, shoots, events, and other places.

Business property insurance is limited to your business premises (there is typically a 500-foot coverage radius around the building). If you typically take your tools, gear, or equipment with you off-premises, you should consider inland marine insurance (also known as Tools & Equipment Insurance), which protects commercial property in transit.

Looking for a deal?

A business owner’s policy, also known as a BOP, combines general liability and business property insurance into a single package policy. You get better protection at a lower price than by purchasing each coverage on its own.

Another great thing about business owner’s policies is that it’s easy to tack on many other endorsements (Non-insurance speak: You can easily add extra coverage to a BOP.)

Workers’ compensation

Also known as workers’ comp, or workman’s comp, this type of insurance is great for self-employed business owners with or without employees. Workers’ comp helps cover expenses incurred due to an employee’s job-related illness or injury.

Examples of such expenses include medical costs and lost wages due to taking time off work to recover. This policy not only protects your employees, but it protects your business as well. Medical costs can be extremely expensive. Paying for them out of pocket could potentially hurt your business, or maybe even sink it.

Workers’ comp policies aren’t always optional. Many states require employers to have the insurance by law. But you should consider workers comp even if you don’t have employees.

Business auto insurance

You need this if your company owns vehicles. Why? If you are driving your car for a work-related reason (even something like errands) and something happens, your personal auto policy typically will not cover the incident.

Learn more about business auto insurance.

Hired & non-owned auto insurance

This kind of auto insurance provides liability protection for vehicles you borrow, rent, or hire. It also pertains to employees who use their personal vehicles on behalf of your business.

Learn more about hired & non-owned auto insurance.

Umbrella Insurance

Do self-employed business owners need umbrella insurance? It depends. Umbrella insurance is also known as excess liability insurance. Insurance policies have limits on how much they will cover if something bad happens. Umbrella insurance boost the limits of your existing policies.

So if you have extra liabilities that your company may face, then yes, you should consider this policy, as it can help pay for the extra expense of unexpected disasters that could put you out of business.

For example, let’s say your business auto policy covers up to $500,000 in damages. You’re in an accident, whose costs add up to $650,000. With umbrella insurance, the additional $150,000 could be covered by your policy. Otherwise, you’d have to pay it out of your own pocket.

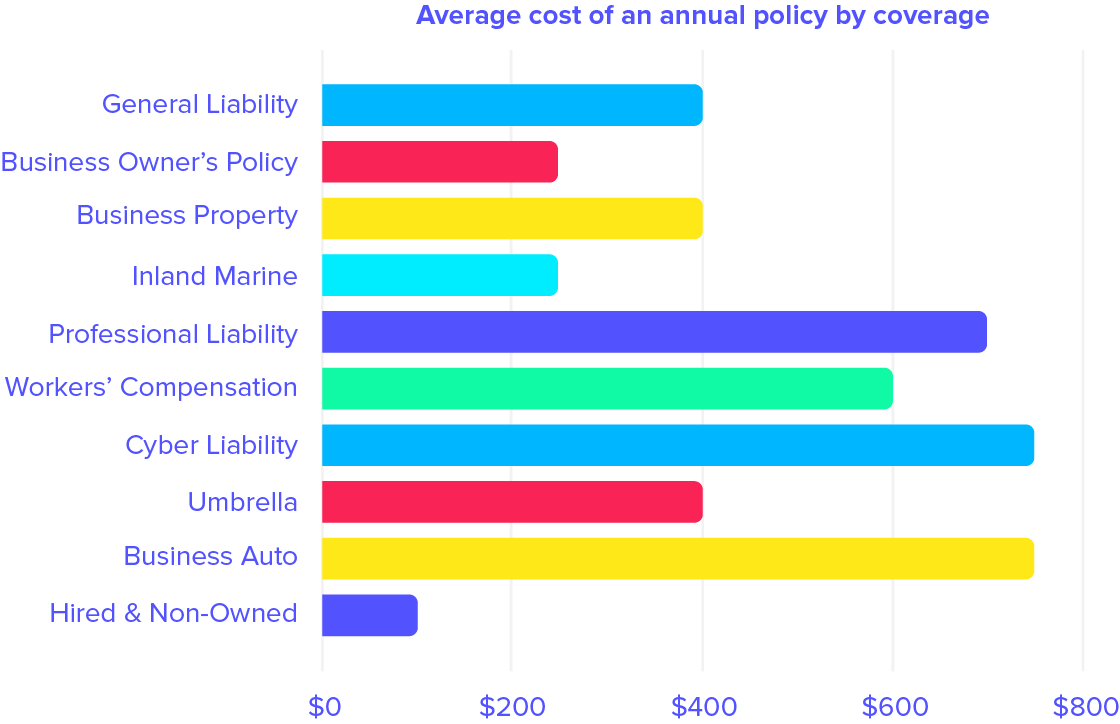

How much is business insurance for the self-employed?

It doesn’t cost as much as most people think. The price of business insurance depends on how much risk you face. For example, a data entry professional will pay much less than a large corporation.

The price of your insurance plan will depend on things like your profession, the size of your business, and the kinds of things you want to protect.

A small self-employed business might pay around $500-$900 a year, while a large corporation could pay over $50,000 a year.

Check out our self-employed insurance cost analysis to learn more.

We can save you money.

We compare over 30 top insurance providers (for free) to find you the right coverage at the most affordable cost. No hidden fees and no obligations.

There are so many variations when it comes to commercial insurance that best way to figure out exactly how much it will cost you is to complete a simple online form about your business, and our experts will show you the most affordable options for your operation.

Comprised of experts with over 30 years experience, we work with top national insurance companies to provide the most competitive rates to our customers.