As a working professional, you want to prove your small business is reliable. You also want to be sure your clients are always protected. While small business insurance can cover you, your employees, your clients, and/or a third party if a property damage or liability claim is ever filed against your small business, sometimes you need more than insurance to protect you and your clients from the unknown.

Surety bonds are one of the best ways for you to build a layer of trust between your business and your clients. Basically, a surety bond assures that your clients will be 100% satisfied with the quality of your work and if for some reason they are not, they will be made financially whole. Some professions even require a surety bond before getting a license or permit.

Want to attract new clients? Surety bonds will make you stand out from your competition!

How do surety bonds work?

A surety bond is a simple written agreement that guarantees that you as a professional worker will perform your job both efficiently and expertly. It helps protect your clients from financial loss, which means if you do not, cannot, or inadequately perform your job, surety bonds ensure payment to the client if a claim were to be filed against you. Many of today’s clients require surety bonds before hiring, which is included in their contracts.

Surety bonds are purchased in set terms, with most insurance companies offering up to four-year terms. Surety bonds can be renewed when needed.

There are three different parties involved with a surety bond:

Principal – the person who purchases the bond; they must make good on the obligation

Obligee – the person who needs the guarantee; the receiving party

Surety – the insuring company guarantees the principal will meet their obligation to the obligee

Surety bonds may be required to:

Comply with a client contract

Comply with a government contract

Legally conduct business for certain professions

Help assure clients that a business is trustworthy

Surety bonds differ from small business insurance:

Business insurance pays claims to the person who holds the policy, while surety bonds pay claims directly to the client

Business insurance policies do not need to be paid back, while surety bonds must be paid back

Types of surety bonds

There are many different types of surety bonds available, making it a good idea for you to fully understand your choices. Need a little bit of guidance? Feel free to contact one of our Pogo insurance specialists for expert advice. CONTACT PAGE?

Contract bonds – Insures a small business will meet and perform all contract terms

Bid bonds

Performance bonds

Payment bonds

Warranty bonds

Commercial bonds – Required by the government, ensures performance

License and permit bonds

Miscellaneous bonds

Fidelity bonds – Helps protect small businesses from financial losses due to things like theft or fraud

Employee dishonesty bonds – Helps protect small businesses from financial losses due to one or more employees exhibiting dishonest behavior

Janitorial bonds – Covers cleaning companies if an employee happens to steal from a client

Business service bonds – This type of surety bond protects customers from potential employee fraud

What do surety bonds cover?

How do surety bonds protect your small business and the obligee from the unknown?

Surety bonds guarantee coverage when a business fails to:

Properly complete a project

Properly meet standards or regulations

Get the proper license or permits

Prevent an employee from stealing

Example: Your small business is hired by a local government agency to build a small structure. The agency wants the work completed in two weeks. If for some reason you are not able to finish the project in time, your surety bond will pay any financial consequences due to the delay. You will then need to pay this amount back to the surety bond.

What is excluded?

Surety bonds do not cover everything, making it necessary for small business owners to also purchase business insurance to make sure they are properly protected.

Surety bonds do not cover:

Who needs surety bonds?

Surety bonds are often required for regular contracting jobs and definitely required for high-cost government contracts. As a professional worker, know that surety bonds are legally binding and you can use them in any type of contract.

Most states require the following professions get bonded before they can legally conduct business:

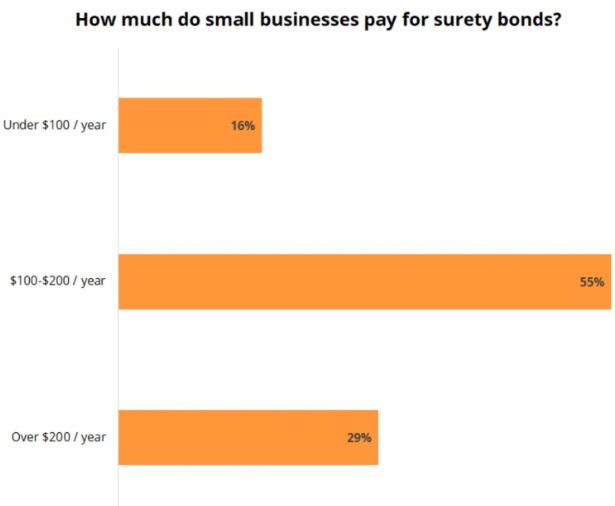

When it comes to how much you will need to pay to get a surety bond, it depends on the risks associated with the project at hand. Know that the majority of small business owners pay somewhere between $100 and $200 annually to get surety bond protection. About one in six pay less than $100 annually. Generally speaking, you can expect to pay somewhere between 1% and 3% of the contract amount for a small business surety bond.

Top questions that determine your surety bond premium:

What size bond do you need?

What type of bond do you need?

How much experience do you have?

What is your personal credit score?

What is your financial history?

TIPS

Learn about the different types of surety bonds so you can make the right choice

Read the surety bond laws in your state

Be prepared – know your credit score, know how much surety bond coverage you need

Know exactly what is included in your surety bond so you can completely understand your obligations

Read the bond before purchasing and signing

Know your coverage start and end dates

FAQsHow long does it take to get a surety bond?

It depends on the type of surety bond you need. Typically speaking, you can have a surety bond in hand within a week after applying.

Can I get a surety bond with bad credit?

Yes, it is possible for you to still get a surety bond when you have a low credit score. Understand that you might need to pay more due to your poor credit history.

Can I cancel a surety bond?

While it is possible to cancel a surety bond, it is unlikely that the cancellation will end up in a refund. Cancellation policies vary from state to state, making it necessary for professional workers to check the policy of their state before purchasing a surety bond.

Surety bond quotes for small businesses

We offer free online quotes from more than 30 top insurance carriers. Simply fill out our three-minute form so we can let you know how much you will need to pay for a surety bond.

Got questions? Please do not hesitate to contact us as we are here for you!